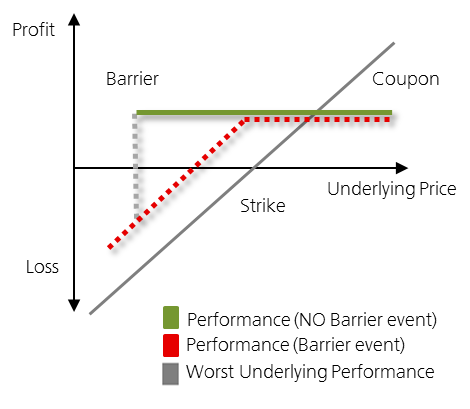

Example

Some investors purchase a barrier reverse convertible on a stock with a barrier of 80% and a coupon of 5%.

If the share price rises significantly, investors will not participate in this performance but receive the coupon.

So, in the case of significant positive performance of the underlying, investors will be better off holding the underlying rather than the barrier reverse convertible. This is why the product is intended for sideways-trending market expectations.

If the stock only declines slightly during the lifetime of the product, e.g. by 15% and does not breach the barrier, then investors holding the barrier reverse convertible benefit from the conditional downside protection and receive their invested capital back at maturity as well as the coupon.

So, in the case of a flat or slightly negative performance of the underlying, they will be better off investing in the barrier reverse convertible based on the conditional downside protection and coupon that it provides.

If the stock drops 30% during the lifetime of the product and the barrier has been breached, the conditional downside protection would be lost. As a result, investors will be fully exposed to this negative performance and only receive back, at maturity, the price of the underlying or the predefined number of shares, unless the underlying fully recovers. However, they will receive the coupon which is usually more than any dividends that the underlying would have paid.

So, in the case of a significant negative performance of the underlying, investors would be better off with the barrier reverse convertible compared to holding the underlying directly due of the coupon paid by the note.